Ever since the Covid-19 pandemic, Canadians have heavily relied on the comfort and utility of their home. Now more than ever, it is crucial that people are living in a home that provides them happiness. According to Statistics Canada, Home renovation spending from February 2021 to June 2021 has drastically increased by 66%, this number has likely maintained since then. According to Statista, when it comes to funding these renovations 58% of homeowners rely on their savings. Within that, 34% are planning to take out a loan to help cover the costs. A loan can not only finance the original renovation but can help control the uncertainty of the project.

Why Renovate Your Home and How Much Will It Cost?

There are many reasons someone would renovate their house:

- To upgrade the comfortability of the home

- To increase the value of a property

- To make it easier to live and work in the same space

- To rent out a portion of the house

- To prepare to sell a home

There are several factors that contribute to the overall cost of a renovation.

- Size of the home

- Location

- Complexity of project

- Age of the home

- Design choices and materials used

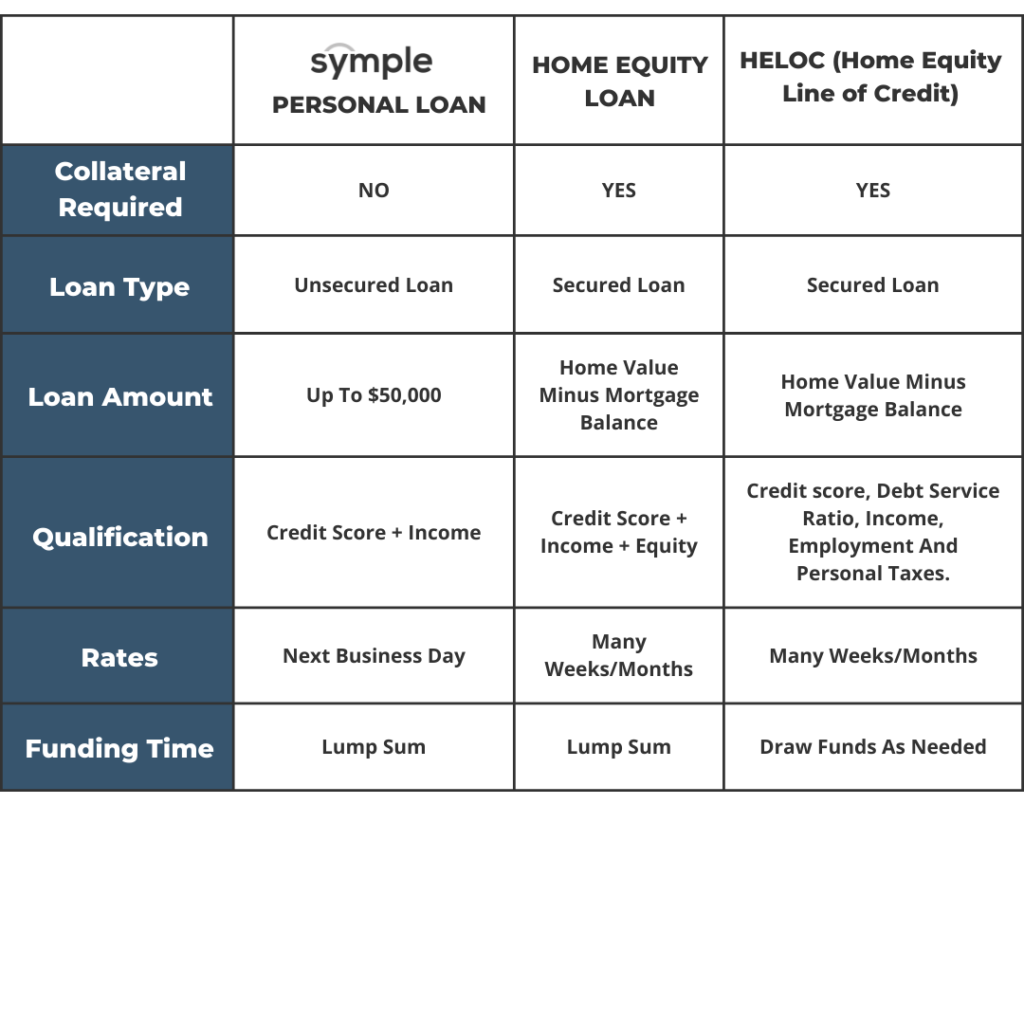

It is recommended to budget for a minimum of $15 up to $60 per square foot. When looking to finance home improvements these costs there are three major types of loans to consider, a Home Equity Loan, a Home Renovation Loan, and a Home Equity Line of Credit. Take a look at the chart below to find out which one is right for you.

What is a Home Renovation Loan and When to Consider Financing?

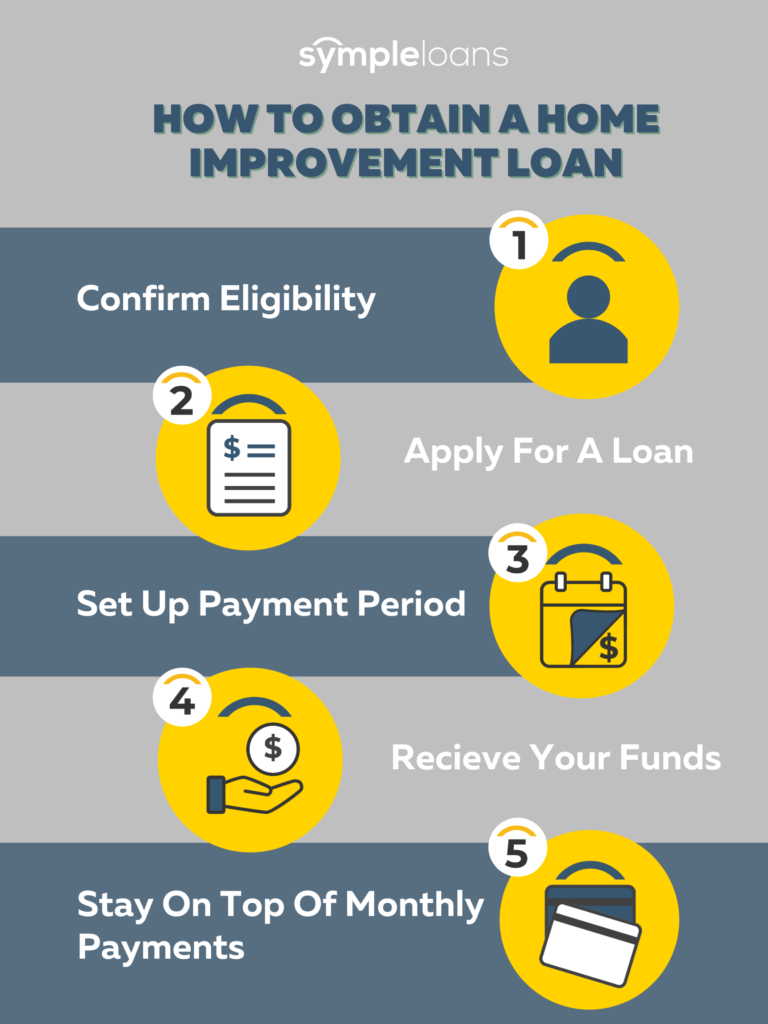

Whether you’re looking to change the flooring or remodel an entire room, a home renovation loan can provide you with the funding to do so. Renovations usually involve a lump sum of money in a brief period of time, which can be hard to budget for. A property renovation loan can help aid a smooth financial recovery. If approved for this type of loan you receive the entire funds at once. You will then repay the loan along with interest on a specific schedule. A home renovation loan provides flexibility as they usually run from 6 months to several years. These loans have a faster and easier application process compared to other financing options. Your eligibility for a Home Improvement Loan depends on your credit score, income, and employment. It is crucial to understand the repayment structure of the loan to ensure you are able to budget for it.

How Does a Home Renovation Loan Work?

Home Renovation Financing can be used for all areas of a home. It provides funds for a large purchase and a set timeframe to repay the loans. These timely payments include lower interest than a credit card.

What are the Benefits of Home Renovation Loans?

Home Renovation loans can not only help aid your home project financially but can provide many other benefits such as:

- Increasing your return on investment

- Flexibility on terms and payment

- Lower interest rates

- Fast approval times

- All funds are disbursed upfront

Repaying Your Home Renovation Loan

Once you have received your funds it is important to understand the repayment procedure. It is best to set up a payment schedule to avoid a default. A default is the failure to pay back a loan under the current agreement. To stay on top of payments it is crucial to curate a schedule that works for you. Repayment periods can be as little as 6 months to several years, with weekly to monthly payments. Understanding these terms ensures you do not miss a payment.

References

www.150.statcan.gc.ca/t1/tbl1/en/cv.action?pid=3410017501

www.statista.com/statistics/932832/how-homeowners-fund-renovation-projects-canada/

www.newswire.ca/news-releases/canadian-homeowners-continue-to-cut-back-on-home-renovation-spending-in-2019-cibc-poll-833298553.html